Life Cycle Costs for Environmental Projects

By Dan Melamed, CCP EVP FAACE

Member AACE Technical Board

National Capital Section Director

The cleanup of contaminated sites involves removing hazards to human health, safety, or the environment from specific building(s) and/or a parcel(s) of land that includes contamination that may have spread to surface and/or groundwater. The nature of this is fundamentally different from most other capital asset projects in many aspects. For capital asset projects, project teams analyze the capital costs of facility planning, design, and construction through start-up of an asset combined with the costs to operate, maintain, and eventually dispose of the asset to give the total cost of ownership of the asset. This analysis is called the life cycle cost analysis (LCCA). However, the analogous LCCA of environmental restoration projects operates from fundamentally different perspective from capital assets (discussed below)

- The environmental cleanup is not generating an asset but eliminating a liability;

- The understanding of the site’s scope, compared to other industries, has a high degree of uncertainty.

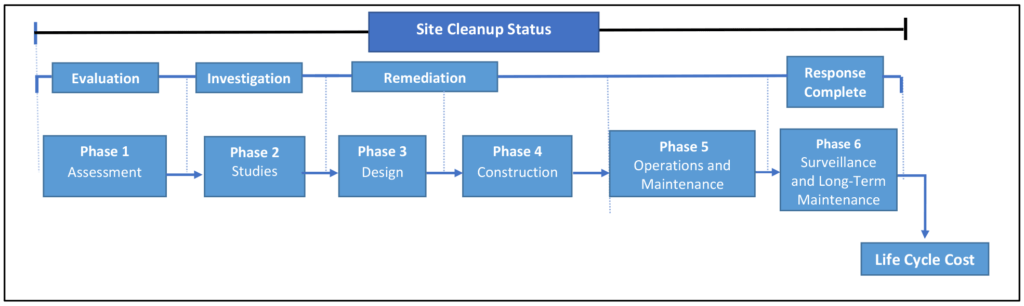

An environmental cleanup follows a distinct sequence of phases (shown in figure 1, which show the life cycle of an environmental project through six phases. (1)

Figure 1–The Six Phases Required to Complete an Environmental Project combining to provide a life cycle cost.

In many (if not most) cases the environmental cleanup is driven by a legal and regulatory framework. It is worth noting that as an example the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA) requires a life cycle cost analysis in order to compare remediation alternatives. Although this is a formal requirement for CERCLA, its general utility for general best practices is directly aligned with best practices for general project and program management. The driver for the environmental legal and regulatory framework is protection of human health and the environment. Therefore, there must be a balance between cost effectiveness with protecting both human health and the environment throughout the life cycle of environmental remediation. Also, as stated above, there are significant uncertainties to environmental cleanup projects. The specific extent and nature of the contamination is almost always uncertain. The dispersion and transport of these contaminants through the environment (even after initial characterization) which can be defined but are difficult to accurately predict quantitatively.

Despite the fundamental differences between the constructing, operating and the eventual disposal of a capital asset and an environmental cleanup, the methods for developing a life cycle cost analysis are the same. Both evaluate a series of approaches to either develop an approach to develop a capital asset or (as discussed in this paper) develop a technological approach for cleanup. The methodology is to account for the time value of money, that is, the variation in the cost of an expenditure due to its timing and the specific nature of the expenditure. This well-established methodology to convert future lump sum values, a uniform series of future values, or an incremental series of future values to a present value. Ultimately one should use the same general methodologies which apply to all industries. (2) These steps are listed below with some considerations for projects in the environmental remediation industry:

- Define the cleanup project requiring LCCA. This step involves characterizing the contaminated site. Identify the potential time periods to be considered in the analysis. Identify the appropriate financial or other criteria upon which to base a necessary course of action. This includes necessary actions (including possible short term removal actions) to contain the further spread of contamination.

- Develop potential alternatives/solutions to consider in the analysis. For this step past experience determines viable technology approaches for the cleanup work. These should be built upon available past experience(s) of previous cleanup activities for similar sites that best address both the nature of the contamination (e.g., radioactive and/or toxic metals) as well as the medium (e.g., concrete for a building, versus clay and/or sandy soils) as well as whether the contamination has migrated (e.g., whether the contamination had traveled to adjacent properties, etc.

- Develop/use an appropriate cost breakdown to support the analysis. The cost breakdown structure for this analysis needs to be based on the environmental industry’s unique requirements including acquisition costs (e.g., planning, procurement, construction) and sustaining costs (e.g., operating costs, utility costs, maintenance costs, repair costs, etc.). A good example of a cost breakdown structure for environmental projects is the Environmental Cost Element Structure (ECES) a comprehensive, hierarchical list of cost elements (tasks, items, or products) that may be required to complete an environmental project. (3)

- Collect data and information to support the required cost and benefit values for each alternative information to determine reasonable estimates for all stages of the remediation.

- Prepare the cost profiles for each alternative

- Analyze results. Analyze the results for the top four to six alternatives, including the preferred alternative, in a formal document(s). Continuing with the example (discussed above) in a CERCLA project this step is entitled the Remedial Investigation/Feasibility Study. (RI/FS).

- Communicate results and determine the course of action. In the case of a CERCLA project, the RI/FS report is distributed with stakeholders (including regulators). Based their review of these documents (including stakeholder input documented at public meetings) a selected remedy is summarized in the record of decision.

The following is an example of a detailed discussion showing a comparison of alternatives on a life-cycle cost basis. [4] There are two possible remedies for the treatment of buried waste:

- Contain the contamination on- site and leave it in place; versus

- The complete removal and disposal of the contamination off-site

Containing the contamination and leaving it in place may have a lower initial cost compared to excavating, characterizing, transporting and disposing of the waste. However, the first remedy requires an engineered cap to prevent migration as well as continued monitoring of groundwater for an extensive period to detect any migration of contamination or changes in contaminant concentrations. Therefore, life-cycle costing can accurately compare these cleanup alternatives.

Another challenge in a LCCA for an environmental project involves calculating long term surveillance and long-term maintenance (SLTM) (also referred to as long term surveillance or long-term stewardship), shown as Phase 6 of Figure 1. These activities may last for many years. Although these costs are often accurately estimated. However, very often there is uncertainty as to how many years these activities will need to be performed, creating uncertainty in the estimated costs for this phase.

A life cycle cost analysis is a critically important requirement for the selection of a remedial alternative and development of an environmental remediation project. Very often the conduct of the LCCA process can help the project team to provide a full understanding of the engineering and technological challenges faced by environmental cleanup projects.

Disclaimer: The content provided by the author of this article is his own and does not necessarily reflect that of their employers, unless otherwise stated.

References:

- AACE International, Recommended Practice No. 107R-19: Cost Estimate Classification System – As Applied in Engineering, Procurement, and Construction for the Environmental Remediation Industries, Morgantown, WV: AACE International, Latest revision. Pages 4-7.

- Larry Dysert. Life Cycle Cost Analysis Source, No. 06, AACE International, Morgantown, WV, December 2018. Pages 6-7.

- ASTM E2150-17, Standard Classification for Life-Cycle Environmental Work Elements-Environmental Cost Element Structure, ASTM International, West Conshohocken, PA, 2017, www.astm.org (with Adjunct E-2150A, which provides Environmental Cost Element Structure at Levels 3, 4, and 5 with Definitions).

- A Discussion of the Cost Estimate Classification System: As applied in the Engineering, Procurement, Construction and Operations for the Environmental Remediation Industries, Dan Melamed, CCP EVP; Bryan A. Skokan, PE CCP; Gregory Mah-Hing, PE; Rodney Lehman; Jake Lefman, 2020 AACE International Transactions, EST-3542, AACE International, Morgantown, WV, 2020. Page 8.

Rate this post

Click on a star to rate it!

Average rating 5 / 5. Vote count: 1

No votes so far! Be the first to rate this post.